The landscape of Commercial Auto Liability insurance in the U.S. is shifting dramatically, driven by a combination of social inflation, nuclear verdicts, and evolving litigation practices. For insurers, policyholders, and risk managers, understanding these forces is no longer optional—it’s critical for survival.

The Unprecedented Rise of Liability Risk

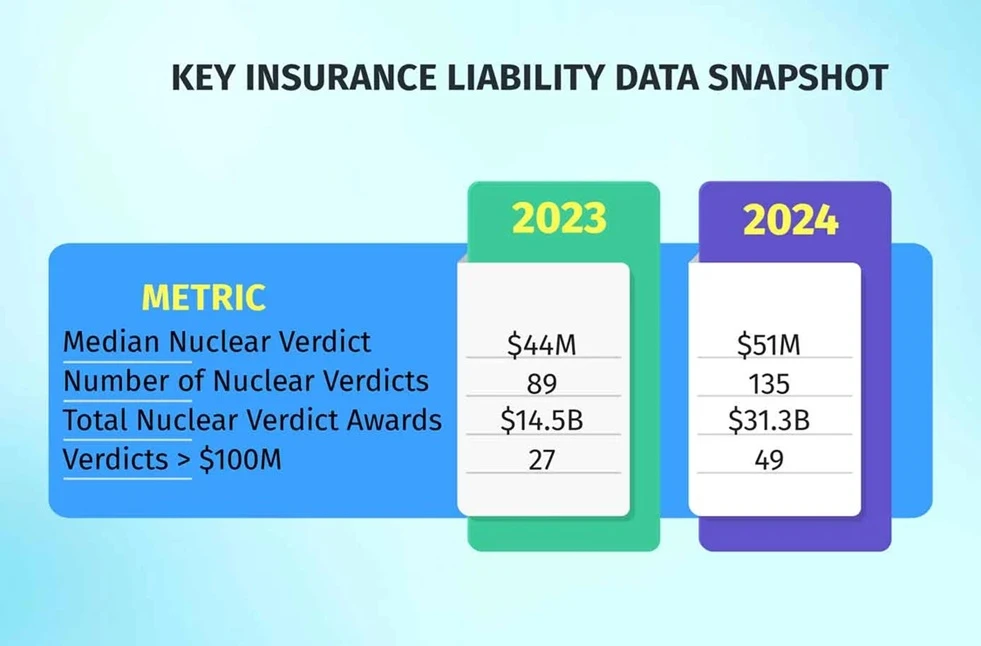

Over the past decade, U.S. liability claims costs have surged by 57%, largely fueled by nuclear verdicts—jury awards exceeding $10 million. Social inflation, a term describing claim cost increases that outpace general economic inflation, plays a central role. Today, social inflation is nearly double the pace of consumer price inflation, and its impact is particularly pronounced in lines like Commercial Auto Liability, general liability, and umbrella insurance.

Unlike property insurance, which is influenced by physical damage and supply-demand dynamics, liability coverage is sensitive to legal trends, juror psychology, and litigation strategies. Juries are increasingly willing to deliver punitive damages as a “message” to corporations. Younger jurors, now nearly two-thirds of panels, are especially inclined to penalize companies perceived as negligent or indifferent to public safety.

Third-Party Litigation Finance: A New Catalyst

A less widely discussed but highly impactful trend is third-party litigation finance. Institutional investors—ranging from hedge funds to private equity—are backing high-stakes lawsuits using advanced analytics to assess potential jury awards. This influx of capital enables plaintiffs to sustain prolonged legal battles, escalating both the frequency and severity of claims. For commercial auto insurers, this trend means that even cases involving moderate negligence can balloon into multi-million-dollar settlements.

Why Commercial Auto Liability is a Hotspot

Commercial Auto Liability is particularly vulnerable because claim severity is closely tied to rising physical and medical costs. Since 2020, medical treatment costs have increased 38% and vehicle repair costs 40%, according to Swiss Re Sigma Report (2024). These increases elevate base claim values, which juries often multiply in their awards.

Certain jurisdictions amplify this exposure. Plaintiff-friendly states like Texas, California, and Pennsylvania have seen a disproportionate number of nuclear verdicts due to limited damages caps and tort reform rollbacks. In 2024 alone, Texas recorded 23 verdicts exceeding $10 million, including multimillion-dollar negligent hiring cases. For insurers, these high-risk regions necessitate careful policy structuring, pricing adjustments, and strategic capacity deployment.

The Litigation Playbook

Modern plaintiff strategies, such as the “reptile theory”, tap into jurors’ emotional responses by portraying corporate defendants as threats to community safety. Combined with heavy litigation advertising—$2 billion spent in 2023—this approach primes juries for larger awards and intensifies social inflation pressures. In commercial auto liability claims, this can transform a straightforward accident into a courtroom battle lasting years, with financial exposure far beyond traditional coverage limits.

Policy Implications and Risk Management

Traditional P&C policies, particularly in primary and low-to-mid excess layers, are being stretched to their limits. Nuclear verdicts over $100 million, sometimes dubbed “thermonuclear,” now regularly breach policy layers once considered sufficient. Insurers are responding by increasing attachment points, tightening policy terms, and occasionally withdrawing from high-risk sectors altogether.

For businesses, the message is clear: maintaining adequate Commercial Auto Liability coverage is no longer just a regulatory or contractual obligation—it’s a strategic necessity. Risk managers must actively evaluate their exposure, consider higher limits or umbrella policies, and engage in proactive safety and compliance programs to reduce claim likelihood.

Conclusion

The rise of social inflation, nuclear verdicts, and litigation finance is fundamentally reshaping Commercial Auto Liability insurance in the U.S. Companies can no longer rely on historical claims data alone; they must adopt forward-looking strategies to protect themselves against extreme, unpredictable losses. By understanding these evolving dynamics, businesses and insurers can better navigate the new reality of liability risk—before the next multimillion-dollar verdict hits.