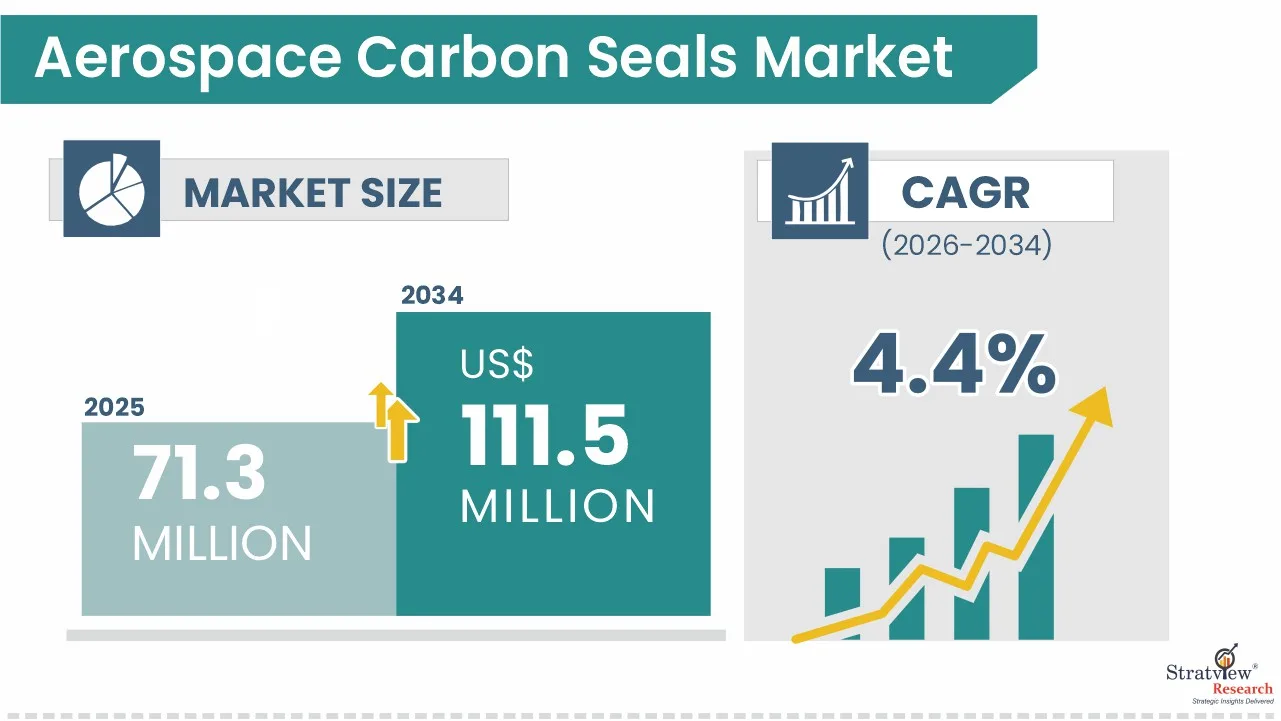

The Aerospace Carbon Seals Market was valued at USD 71.3 million in 2025 and is likely to reach USD 111.5 million by 2034. The market is expected to grow during 2026-2034, supported by a CAGR of 4.4%.

The Aerospace Carbon Seals Market Forecast points to steady expansion supported by commercial aircraft demand, turbine engine applications, and advanced sealing technologies. Forecast visibility is important for suppliers planning capacity, material development, and customer alignment. The market’s outlook reflects the continued need for reliable components in high-temperature, high-speed aerospace environments.

Carbon seals are manufactured from carbon-graphite materials and are used in aircraft engines, auxiliary power units, and gearboxes. They help prevent leakage of lubricants, gases, and air across rotating shafts and bearing compartments.

The key growth driver is increasing aircraft production, expansion of the global fleet, and rising maintenance, repair, and overhaul activities. As aircraft fleets expand and utilization increases, demand rises for sealing systems that support engine efficiency, operational safety, and system durability.

Request a free sample report: https://www.stratviewresearch.com/Request-Sample/4594/aerospace-carbon-seals-market.html#form

Market Segmentation Analysis

By Platform Type

- Commercial Aircraft (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

- Regional Aircraft (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

- Helicopter (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

- Military Aircraft (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

- General Aviation (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

- Space (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

By Application Type

- Turbine Engine (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

- Auxiliary Power Units (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

- Gearbox (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

- Hydraulics & Actuation (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

- Other Applications (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

By Product Type

- Face Seals (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

- Circumferential Seals (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

- Other Products (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

By End-User Type

- OE (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

- Aftermarket (Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

By Region

- North America (Country Analysis: The USA, Canada, and Mexico)

- Europe (Country Analysis: Germany, France, the UK, Russia, and the rest of Europe)

- Asia-Pacific (Country Analysis: Japan, China, India, and Rest of Asia-Pacific)

- Rest of the World (Country Analysis: Brazil, Saudi Arabia, and Others)

Commercial Aircraft account for the largest share of the market and are also projected to witness the fastest growth. Their large global fleet size, high utilization rates, and frequent MRO requirements increase the need for carbon seals in engines and auxiliary systems. The strategic implication is clear: demand remains closely tied to fleet expansion and aircraft production cycles.

Turbine Engine holds the dominant share, while Auxiliary Power Units are likely to be the fastest-growing application. Carbon seals are used in turbine engines for multiple rotating interfaces and high-temperature sections. APUs gain from aircraft deliveries, onboard power reliability, and MRO activity. This positions sealing demand around core propulsion and auxiliary power systems.

Face Seals dominate the product type segment and are projected to register the fastest growth rate. Their sealing efficiency, high-pressure capability, and high-temperature operating performance support use in critical engine sections, bearing compartments, oil systems, and gearbox compartments. This indicates sustained demand for reliable sealing solutions in high-speed rotating environments.

OE accounts for the largest share, while the aftermarket segment is likely to grow steadily. OE demand is linked to aircraft engines, APUs, and gearboxes integrated during initial assembly. Aftermarket demand increases because carbon seals face wear from heat, pressure differentials, and rotational stress. The strategic implication is a dual demand base across production and replacement cycles.

Explore the latest market analysis and forecasts for the Aerospace Carbon Seals Market:

https://www.stratviewresearch.com/4594/aerospace-carbon-seals-market.html

Regional Market Insights

North America dominates the aerospace carbon seals market. The region’s position is supported by the strong presence of aircraft OEMs, engine OEMs, tier players, and extensive MRO infrastructure. A large installed fleet and high aircraft production rates create sustained demand across both OE and aftermarket segments.

Asia-Pacific is emerging as the fastest-growing region during the forecast period. Growth is supported by rising air passenger traffic, increasing aircraft fleet size, aircraft procurement, defense spending, indigenous aircraft programs, and expanding regional MRO capabilities. These factors increase demand for replacement components, including carbon seals.

Emerging Trends Shaping the Aerospace Carbon Seals Market

The Aerospace Carbon Seals Market is being shaped by material and performance-focused development. Industry players are concentrating on improving leakage properties, increasing seal life, and enhancing thermal properties and wear resistance.

Carbon material improvements are linked to optimized porosity levels and impregnation systems. Segmented ring face seals are also being improved, along with seals for turbine engines, gearboxes, auxiliary power units, fuel systems, and oil management systems.

The market forecast reflects steady demand from aircraft production, fleet expansion, and MRO activity. These market trends indicate that carbon seals remain structurally important to engine efficiency, operational safety, and system durability.

Key Growth Drivers of the Market

- Increasing aircraft production supports OE demand because carbon seals are integrated into engines, APUs, and gearboxes during initial assembly by OEMs.

- Expansion of the global fleet increases utilization and operating cycles, creating recurring demand for sealing components exposed to heat, pressure, and rotational stress.

- Extensive MRO infrastructure strengthens aftermarket demand because carbon seals require periodic replacement to maintain leakage control and system durability.

- Advancements in aeroengine technologies increase demand for carbon seals that can operate under higher temperatures, pressures, and rotational speeds.

- The aerospace industry ecosystem, including aircraft OEMs, engine OEMs, tier players, and MRO providers, supports demand across both new production and replacement channels.

Competitive Landscape

Top Companies in the Market

- Eaton Corporation plc

- AB SKF

- Enpro Inc. (Technetics Group)

- Stein Seal Company

- Eagle Industry Co., Ltd.

- Ergoseal, Inc.

- Magnetic Seal Corporation

- St. Marys Carbon Company Inc.

- Morgan Advanced Materials plc

- Ningbo Tiangong Fluid Technology Co., Ltd.

Conclusion and Strategic Outlook

The Aerospace Carbon Seals Market is positioned for steady growth, moving from USD 71.3 million in 2025 to USD 111.5 million by 2034. The market is expected to grow at a CAGR of 4.4% during 2026-2034.

Growth is supported by aircraft production, fleet expansion, MRO activity, and advancements in carbon-graphite materials. Commercial Aircraft, Turbine Engine, Face Seals, and OE remain key demand areas, while Asia-Pacific shows the fastest regional growth profile.

For stakeholders, the market size and industry outlook point to a demand base shaped by both initial aircraft assembly and long-term replacement needs. Carbon seals continue to support engine efficiency, leakage control, safety, and durability across aerospace systems.

FAQs – Aerospace Carbon Seals Market

What is the market size and forecast for the Aerospace Carbon Seals Market?

The Aerospace Carbon Seals Market was valued at USD 71.3 million in 2025. It is likely to reach USD 111.5 million by 2034, growing at a CAGR of 4.4% during 2026-2034.

What are the main growth drivers of the market?

The market is driven by increasing aircraft production, expansion of the global fleet, and rising MRO activities. Advancements in carbon-graphite materials and manufacturing technologies also support demand by improving seal performance and component lifespan.

Which region dominates the market?

North America dominates the market. Its leadership is supported by aircraft OEMs, engine OEMs, tier players, extensive MRO infrastructure, and a large installed fleet of commercial and military aircraft.

What is the investment outlook for the market?

The investment outlook is linked to steady growth across OE and aftermarket demand. Aircraft production supports new component demand, while MRO activity supports recurring replacement needs over the forecast period.